When you’re settling into your French dream home, the last thing you want to worry about is a legal maze. Most homeowners simply want a job done well, but many are unaware of the core theme of today’s guide: Know the difference: what your handyman is legally allowed to do (and what requires an artisan). There is a massive legal and insurance divide between these two roles. It isn’t always about who is better with a wrench; it’s about the specific insurance each professional carries, and understanding that distinction is what protects your home when things go wrong.

Many handymen working in France may well have been exceptional, highly-skilled tradespeople back in the UK. However, the French system draws a hard line: unless a professional is registered for a specific trade and carries the mandatory Assurance Décennale, they are legally restricted in what they can touch. Hiring a “jack-of-all-trades” for a master-level job might seem like a win today, but it can become a heartbreakingly costly exercise if an insurance claim is rejected later.

To see how easily this line gets blurred and the consequences of crossing it, let’s look at a situation a homeowner could face.

The story of the uninsured shower disaster

Imagine Mark and Lisa, new homeowners in France, eager to add a shower to a spare bedroom. They hire a friendly, English-speaking tradesperson registered as “homme à tout faire” (handyman). He quotes a modest price, confirming he can “install the plumbing,” which involves running new water lines and waste pipework to the new location. He does the job quickly, and everyone is happy.

Eight months later, a leak develops deep within the wall where the new pipework was installed, causing significant damage to the plaster and the floor below. When Mark and Lisa contact their insurer, the claim is rejected. Why? Because the handyman was not legally qualified or insured to install new pipework, a job that legally requires a qualified plumber and Décennale Assurance. The work was considered a modification to the home’s functional network, and without the proper insurance certificate, the homeowners were left liable for the full €7,000 repair bill.

This story highlights a major, often costly, misconception: in France, a handyman is not a cheap version of a tradesman. Understanding the legal line between the two is vital to protecting your biggest investment.

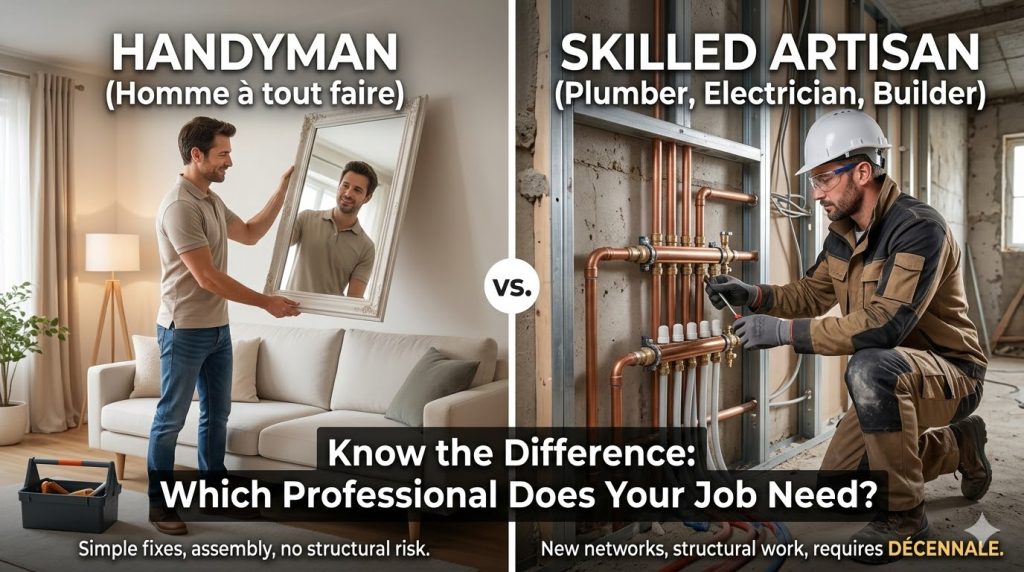

Defining the Legal Line

In France, construction and renovation trades are strictly regulated to ensure safety and quality. This regulation centres around the Assurance Décennale (Ten-Year Guarantee).

The Artisan vs the Handyman: A legal split

| Professional Category | Key Requirement | Work Scope |

| Skilled Artisan | Décennale Assurance (Mandatory) | Trades like roofing, plumbing, electrics – work that affects the structure, water tightness, or main functioning networks of the building. |

| Homme à tout faire | RC Pro only (Professional Civil Liability) | Simple, non-specialised tasks that do not affect the building’s integrity. |

The term Homme à tout faire (handyman or “man for all jobs”) is a common-law or administrative category, but it is not a trade in the same way an Artisan (e.g., plumber, roofer) is. It exists specifically to define work that does not require the ten-year structural insurance (Décennale).

Your handyman’s registration (often under the APE code 81.21Z – Nettoyage courant des bâtiments) permits them to carry out a range of multi-service work that does not require a specific diploma. They are excellent for minor maintenance, but they are severely restricted by law.

The 3 golden rules of handyman work

Your handyman is legally required to stick to tasks that meet all three of these characteristics:

- To be elementary and occasional.

- Not requiring any particular professional expertise (i.e., no specific diploma or qualification).

- Which can be completed in a maximum of two hours.

In other words, the work must be quick, simple, and something an average, competent DIY homeowner could perform.

✅ What your handyman CAN do

A legally compliant Homme à tout faire is perfect for small jobs that improve the look or functionality of your home without touching its core infrastructure.

- Minor fixings: Hanging/removing curtains, fixing a shelf, picture frames, or wall mirrors.

- Assembly: Assembling flat-pack furniture (IKEA, etc.).

- Basic replacements: Replacing a seal, a light bulb, or a gas cylinder.

- Simple maintenance: Cleaning specific floors or surfaces (like using a high-pressure cleaner on a terrace), maintaining a fence or shutters, or installing a simple chandelier.

- Light gardening: Mowing the lawn, weeding, or basic trimming (they cannot operate as a landscaper, sell plants/equipment, or perform heavy pruning/earthmoving).

Crucial note on materials: Handymen are generally excluded from the sale of products or equipment. However, the supply of small items needed for a repair (screws, small brackets, etc.) is permitted, though the maximum amount of DIY expenses eligible for a potential tax credit cannot exceed €500.

🛑 What your handyman CANNOT do

If a job involves the core trades that require a standard of knowledge and skill (and therefore Décennale), it is off-limits. This includes:

- Any work related to plumbing, roofing, main electrics, or masonry.

- Undertaking major construction work such as demolition.

- Work requiring specific qualifications (e.g., handling refrigerants, gas lines).

If a handyman performs these jobs, the work is uninsured, and if a defect arises later, you are financially exposed. Just like Mark and Lisa in our story.

Protecting your investment

As a homeowner, the responsibility to check your professional’s insurance and legal limits ultimately falls to you.

Insist on seeing the appropriate documentation for the specific task at hand. If you are having a new plug socket installed, you need a qualified electrician who can provide a Décennale Certificate for “Electrical Work.” If you are having a picture hung, a handyman with simple RC Pro is fine.

Your protection lies in verifying that the professional’s insurance legally covers the nature of the job they are about to do. If the work is skilled and structural, the insurance must be Décennale. If they provide only RC Pro, the work must be elementary and take no more than two hours.

Remember: Always check the professional’s paperwork against the service you need. It is the only way to avoid the costly “handyman trap” and ensure your French home is built and maintained correctly.

{kind=link}